Introduction

The subprime mortgage crisis of 2008 has largely been blamed because of the poor risk management and misleading selling practices by lender and financial institutions. However, the speculative bubble and its burst was also due to the reckless financial behaviors of households. The lack of awareness among the individuals forced them to rely on unfitted financial advice from relatives or dishonest lenders or even sheepishly follow the irresponsible behaviours of other (OECD, 2009 ). The 2008 financial crisis eroded $11 trillion household wealth alone in the United States1. This essay is not about the financial crisis nor about its impact. The glimpse of financial crisis has been explained to explain the necessity of financial literacy. This essay attempts to explore the role played by financial literacy for the economic development that has mostly been overlooked by policymakers.

What is financial literacy?

Simply, financial literacy means the ability of an individual to manage his/her finances. It represents the level of aptitude in understanding personal finance; awareness and knowledge of key financial concepts required for managing personal finances and is generally used as a narrower term than financial capability (World Bank, 2014 ). Financially literate people have the capacity to make rational financial decisions that is likely to benefit themselves, their society and the economy as a whole. It has three major components: knowledge, attitude, and behaviour (OECD/INFE, 2022 ). Financial knowledge means the knowledge, information about different financial products and services. Financial attitude are the individual characteristics that take the form of tendencies towards a financial practice or action and shows the inclination or likelihood of a person to undertake a behaviour (Ramirez-Montoya, 2017 ). Financial behaviours are the actions one need to exhibit to achieve financial well-being that include: (i) managing their money, (ii) researching and seeking knowledge about financial decisions, (iii) planning and goal setting and (iv) follow-through the first three actions (Long, 2023 ).

How is the situation of financial literacy globally and in Nepal?

S&P Global Financial Literacy Survey 2014 is the most comprehensive global measurement of financial literacy till date which measured the level of financial literacy based on four financial concepts:;(i) risk diversification, (ii) inflation, (iii) numeracy2 and (iv) interest compounding. For this survey, 150,000 adults in over 140 countries were interviewed. The key findings of this survey included:

- Only 33% of adults worldwide are financially literate of which 35% of men and 30% of women are financially literate. Women trail men in financial literacy in both major advanced and emerging countries.

- Risk diversification is the least understood topic among the four mentioned above.

- Though account holders are financially savvy, only 36% of account-holding adults are found to be financially literate.

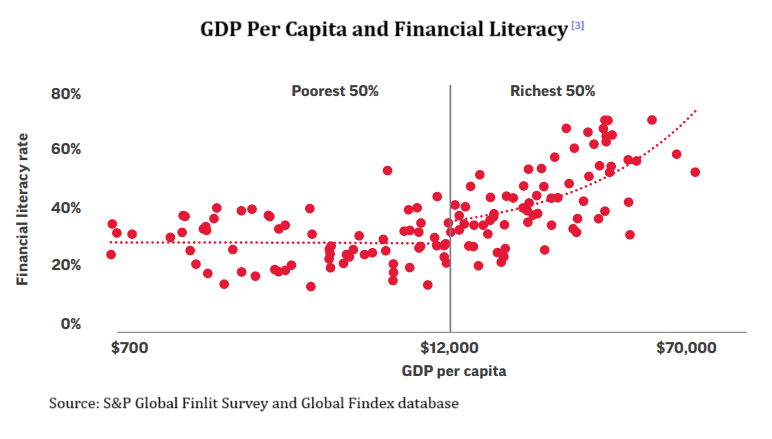

- For richer countries, high economic development is tied with high financial literacy. However, the relationship doesn’t hold true in case of poor countries.

- Young adults are found to be more financial literate than old age people in both advanced and emergin economies.

- Further, financial literacy is found to be have positive relationship with math scores of young population except in Portugal, Vietnam, South Korea and China. Scandinavian countries are found to have higher financially literate population. Norway, Denmark and Sweden had 71% of adults financially literate while the USA had only 57% adults financially literate.

- In the SAARC region, Bhutan has the highest financially literate adult population i.e., 54% followed by Maldives (35%). Nepal has only 18% of adult financially literate while India has 24%.

In the context of Nepal, Nepal Rastra Bank’s financial literacy survey3 conducted in 2022 found that 57.9% of Nepalese of age above 18 years are financially literate. Bagmati province has the highest while Madhesh province has the lowest financially literate population. Males are found to be more financially literate than females by 7.5%. The gender gap in financial literacy score has been found in all provinces with the gap being the widest in Madhesh and Sudurpaschim province. Likewise, Younger people (18-30 years) are more financially literate than older ones (above 60 years).

What role does financial literacy play in an economy?

a. Reduce the risk of systemic failure of financial system

First significance of the financial literacy to an economy could be to reduce the systemic failure of the financial system. Individuals may believe that their financial behavior is based on the rational assessment of the market. However, they may be just exhibiting herd behaviour4 because they are incapable of their own analysis. Such collective actions of individuals can fuel speculative asset price bubbles to unsustainable level or drive down prices beyond the intrinsic value. In 2007, the mortgage-backed securities (MBS)5 were hotcake in the financial market. Both retail and institutional investors had little knowledge on this new investment instrument leading to the mis-selling of the MBS. The misinformation followed by the herd behaviour of investors drove the prices of MBS to levels beyond imagination. When borrowers of housing loans started to default, the value of MBS dropped quickly leading to the collapse of the entire financial system. The shocks of the collapse of major financial institutions were felt throughout the world.

b. Overall economic stability of the country

Empirical evidence suggests that financially literate people tend to have less distorted expectations about economic situations. But why is this important for financial stability? It is because people with less distorted expectations neither are too positive about economic expansions nor are too negative about economic contractions. Their intellectual capability allows them to adapt their actions by judging the economic scenario. This is crucial to reduce the amplitude of the booms and busts. Adam, Marcet and Beutel (2017) explained that typical households in the US are excessively optimistic during booms and pessimistic after busts. However, financially literate investors don’t succumb to such systematic biases (Beutel, 2017) .

c. Corporate Governance

It is a daunting task for regulators to keep a close eye on each company in their jurisdiction because of the resource constraint. However, companies are constantly scrutinized when the public is financially literate. Financially educated investors can function as an important partner for the regulators to overview companies’ policies, practices and procedures to ensure all stakeholders’ interests are balanced. Companies’ best practices are rewarded, which is reflected in their stock price. Additionally, financial literacy can support the securities market regulators by identifying and reporting frauds and scams (OECD/INFE, 2017 ).

d. Financing Resource Gap

Financial literacy can be crucial to raise required investments for the development of an economy. The share of retail investors in global assets under management has reached 51% in 2021 and expected to reach 61% by 2030 according to the strategic consulting firm Indefi. This means the role of retail investors in global investment is going to be huge in the future. Hence, countries should not underestimate the role of retail investors in economic development.

Further, the recent events like global COVID-19 pandemic followed by Russia-Ukraine have shown that it is not reliable to completely depend on foreign investments for economic growth and prosperity.6 Why? Because foreign investors are more sensitive to geo-political tensions or any other misfortunes meaning they could pull out their investment at any time. The growing trend of deglobalization fueled by supply chain disruptions post COVID pandemic could be major evidence. This event should encourage the government to increase the participation of investors in capital market by boosting their confidence through financial literacy. At the same time encouraging local investors participation in domestic capital markets can enhance the depth and make them less dependent on external factors and more resilient to global financial shocks (International Monetary Fund, 2014 ).

e. Individuals’ Financial Stability

From individual perspective, financial literacy plays a crucial role to enhance the financial well-being of individuals. The increasing complexities of financial instrument, inflation and increased risks due to geo-political tensions and climate change have increased the need for financial literacy for individuals for their financial resilience and well-being (Lusardi & Messy, 2023 ). A study by Gerardi, Goette and Meier (2013) found that there was a significant and negative association between mortgage default and numerical ability among the subprime mortgage borrowers who took loans pre-financial crisis of 2007 in the US.

More specifically, financial literacy can enhance the financial well-being in following ways: (i) control the excessive spending habit, (ii) explore different financial instruments for investments, (iii) diversify the portfolio for risk diversification, (iv) better financial planning to set budget aside to meet the current financial needs while keeping certain portion for future contingencies and investments.

Additionally, financial literacy can be crucial to address the risk taking by retail investors. Some investors have excessive risk-taking behaviour who invest in capital market without any precautions. While investors on other spectrum are excessive risk-averse which means they are less likely to participate in capital market or only prefer long-term investment which has low returns (OECD/INFE, 2017 ). Financial literacy can be vital in addressing this issue by giving confidence to risk-averse investors and educating the need of precautionary measures to the risk-takers.

Financial Innovations and Financial Literacy

In the past decade the technological innovation has accelerated in an unimaginable speed. Rapid technological innovation has supported every aspect of the economy. One key product of technological development is financial innovation.7 Individuals are able to use different financial products and services. However, the problem is that the speed of development of complex financial products and services is way faster than people could understand these financial products and services. The result is complexities in making financial decision have increased multiple folds. People with low financial knowledge are subject to greater risk of “financial fraud”. The rationale is that these people have low knowledge on any financial products and services and are likely to be misled to purchase those products and services.

One key example of mis-selling of financial products can be of NFT.8 In early 2021 NFT became so popular worldwide. Especially digital artworks gained huge attention. For example, Beeple’s NFT artwork “First 5000 days” was sold for 69 million USD at auction house Christie’s. People with no knowledge on the underlying mechanism and technology of NFTs followed the NFT trend. They invested heavily in NFTs with celebrity endorsement hoping huge ROI. However, the NFT trend didn’t last long. NFT market trading volume of $24.7 billion in 2022 is projected to shrink by more than 50% in 2023 according to chainalysis. This means people are losing huge sums of money. This recent event depicts the necessity of financial knowledge. One must note that the mis-selling not only affects those who face direct losses but also reduces the confidence of wider population on the whole market reducing investments and liquidity (OECD/INFE, 2017 ).

The Case of Nepal

Financial Access Report 2021 published by Nepal Rastra Bank shows that an estimated 67.3 percent Nepalese have at least one bank account. Similarly, there is massive interest towards the capital market in Nepal in recent years. It is evident by the fact that the number of DEMAT account holders have reached around 58 lakhs by June 2023 as per CDSC database. That is every 1 in 5 individuals has DEMAT account assuming 1 DEMAT account per person. This is a great achievement for a country like Nepal because more and more people connected in the financial system. Does this data suggest the improving scenario of financial literacy in Nepal? May be not. Because (i) most of the Demat accounts of old age people are opened by their grandchildren and children, (ii) apart from initial public offering, very few people are involved in secondary market, (iii) most of the people are still not aware of other financial instruments like mutual funds, bonds and insurance in which they can diversify their portfolio, (iv) people who are involved in secondary market have the tendency to show herd behavior.

Beyond the investor protection, financial literacy is especially important for Nepal to secure the funds to bridge the financing gap. Nepal aims to achieve Sustainable Development Goals by 2030 for which Nepal requires Rs. 585 billion per year according to the World Bank. Financial literacy can help Nepal to bridge this financing gap by encouraging Nepalese participation in the capital market. However, Nepalese authorities haven’t recognized the important role financial literacy can play for economic development. Our financial literacy programs are limited to the celebration of World investor week and Global Money week. Nepalese authorities haven’t developed any broad strategies and plans to improve the financial literacy of Nepalese in regard to growing complexities in financial system. Low levels of financial literacy among Nepalese can be problematic for the country trying to bring more complex financial instruments. May be the authorities should work with the Curriculum development center and include some topics of financial literacy from the secondary school level. Just an idea!

Footnotes

The losses in household wealth in the United States was 8.5 trillion USD in financial assets and 2.5 trillion USD in housing assets during the financial crisis of 2008. See https://www.imf.org/en/News/Articles/2015/09/28/04/53/sonum062409a for more information. ↩︎

Numeracy has been defined as simple interest. For more information, see https://gflec.org///wp-content/uploads/2015/11/ALPrez.pdf . ↩︎

The survey was based on OECD/INFE Toolkit 2022 which measured knowledge, behaviour and attitude dimensions. For this survey, a total of 9361 Nepalese of age above 18 years were selected using multistage sampling method. ↩︎

Herd behaviour is the tendency of individuals to follow others’ actions without their own independent analysis. ↩︎

MBS is a type of asset backed security collateralized by pool of mortgages. ↩︎

It is to note that author completely believes on the strong role of FDI for development. However, the author strongly supports the idea of locally pooled investment more than FDI. ↩︎

Financial innovation is the process of development of new financial products, process, services. ↩︎

NFT stands for non-fungible tokens that are crypto assets used to certify ownership and give authenticity to a digital file that can be image, video, or text. For more information, see https://101blockchains.com/history-of-nfts/ ↩︎